E-commerce had a volatile 2023. From declining sales in luxury to behemoth partnerships to the resurgence of influencer marketing, the last 12 months experienced several changes and surprises that even the analysts were not expecting. Reflecting on the performance and strategies of social commerce platforms, brands and marketplaces in 2023 has set the scene for a fast-moving and competitive market for 2024. Omnia looks at how the previous year ended within e-commerce and what industry players and shoppers may expect in 2024.

Social commerce will show its teeth

Within the e-commerce landscape, it was the expansion of social commerce that made the largest leaps and bounds, proving once again how it has become the largest growing sub-industry within retail and e-commerce with an expected value of $2 trillion in 2025.

Forbes predicted that social commerce is growing three times faster than e-commerce while the moves and counter-moves made in 2023 mirrored why: Meta and TikTok are not interested in your lunch selfies anymore. They’re interested in your likelihood to shop. With Meta’s new partnership with Amazon, allowing Facebook and Instagram users to shop Amazon ads directly in the app, a new era of e-commerce is forming that further increases Amazon’s control of the market and further drives Meta’s plans to create shopping-first platforms.

Other social commerce companies such as TikTok, which is owned by Tencent in China, will also be focusing on establishing itself as a legitimate e-commerce and influencer marketing platform in the West. TikTok Shop’s launch in the US in September is set to disrupt both the social commerce and marketplace arenas for 2024. TikTok and Instagram are each other’s biggest competitors, thickening the hunt for consumer attention and loyalty. Instagram and Facebook are still the world’s top choices over TikTok for buying products, however, the difference is incremental: In Germany, 46% of shoppers use Instagram while 42% use TikTok. In the US, it’s 42% and 40% respectively, and in the UK, TikTok surpasses Instagram as the platform of choice (39% vs 35%). Despite TikTok’s incredible growth and influence, Omnia predicts that Meta’s new Amazon deal will keep them out of the top position for the foreseeable future.

Marketplaces will face stiffer competition with less market share

Niche marketplaces within luxury such as Yoox Net-A-Porter (YNAP), Farfetch and Matches almost ended in collapse in 2023, however, Farfetch was saved by South Korea’s e-commerce giant Coupang in a last-minute sale, Matches has been purchased by UK retailer Frasers for €60 million, while YNAP is still searching for a saviour to bring them into the black since the sale to Farfetch fell through.

According to Vogue Business, Amazon or Alibaba could potentially purchase YNAP, two of the world’s biggest e-commerce platforms, further strengthening their grasp on the marketplace landscape. As mentioned above, Amazon has continued its growth and consolidation by entering the social commerce space with Meta, which was announced in November, and the results of this deal will play out interestingly throughout 2024.

How will this affect other marketplaces? In 2024, marketplaces will feel the pinch of the Meta-Amazon coalition as an increasing number of lucrative vendors will turn toward Meta platforms to make sales and grow their brands. As a result, consumers will go where there is variety with a competitive price and an easier shopping experience. However, if more shoppers will be heading toward Meta platforms, marketplaces may be able to take advantage of the increased traffic with new advertising, sales and pricing strategies. Marketplaces other than Amazon will need to incentivise shoppers to choose their platform - whether it is via social media or not - to remain profitable.

Although Zalando ended off 2023 with declined quarterly sales, their new partnership with Highsnobiety has led Omnia to believe that they too have noticed the e-commerce success that lies within content. Europe’s largest marketplace has realised that many customers, especially Gen Z and millennial shoppers, buy into content and not products. The new platform, entitled Stories, creates fashion-related video content and provides news of collaborations and interviews with designers. “We know that customers are looking for inspiration and with Stories on Zalando we are doing exactly that: crafting highly engaging formats to show what’s new and what’s next in fashion,” says Zalando’s Senior Vice-President of Product Design Anne Pascual.

Brands will restrategise marketing and sales strategies to regain sales

Brands in multiple categories, especially in fashion, beauty and luxury, experienced a cooling period in 2023 that lasted longer than expected. For some, this will extend into 2024: Burberry’s shares have dropped 15% after they reduced their profit outlook thanks to a quieter-than-expected sales period over Christmas. Nike is cutting jobs and is set to reduce $2 billion in costs over the next three years amid dwindling sales. Gucci’s brand equity dropped 31% from 2022 to 2023, while L’Oréal and Lancome list 20% and 19% respectively.

Overall, the annual Kantar BrandZ report concluded that the world’s top 100 brands lost 20% of their value in 2023, leaving them on the back foot as 2024 gets underway which will see brands moving and shaking to get into a profitable, growthful place again.

Despite the overall lookout, other brands in some verticals including sports apparel and performance footwear did well such as Swiss-owned running shoe maker On which saw third-quarter sales increase by 44% and HOKA, which consistently saw growth throughout 2023 and gained in market share.

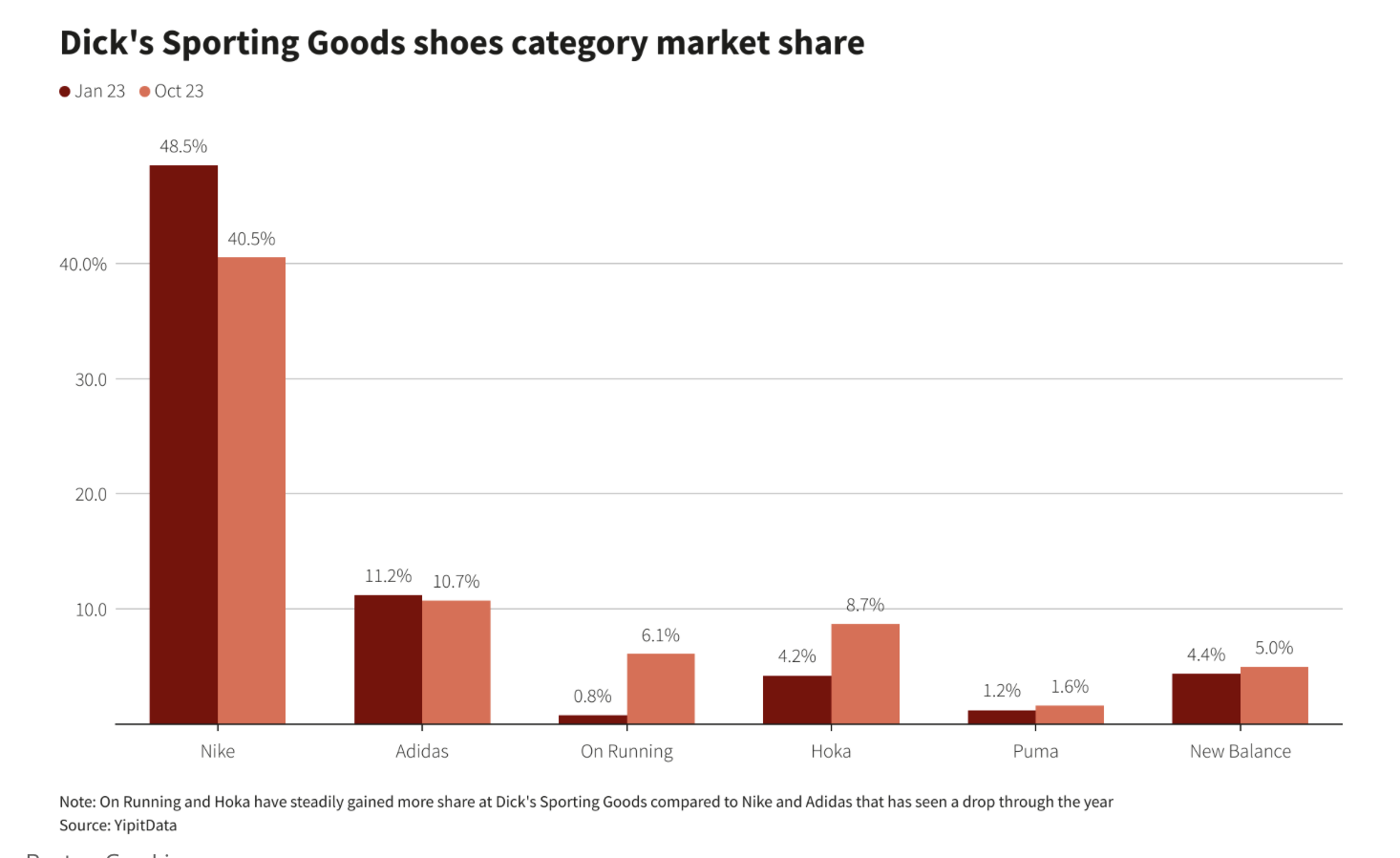

In 2024, On is focusing on building its D2C channel which will cut into market share controlled by Adidas and Nike which have seen declining market share at Dick’s Sporting Goods, one of the US’s largest shoe retailers, while On and HOKA increase.

2024 trends in sports apparel include a transition from logo-heavy designs, which we saw gain prevalence within “quiet luxury”, to “quiet outdoors”. Brands like North Face and Arc'teryx will be focusing on gaining the attention of luxury buyers who want in on sportswear with a high-end feel.

Looking forward to 2024

In the four years since the start of the Covid-19 pandemic, e-commerce and retail have experienced a decade of rollercoaster highs and lows. The resilience of both consumers and all e-commerce players has paved the way for a more hopeful 2024, however, not without the need for robustness.

The result of a rocky 2023 for brands and marketplaces, including the surprising partnership with Meta and Amazon, will see e-commerce players battle for market share and consumer attention harder than before. They will need to stay agile, embrace innovation, and forge strategic partnerships to thrive in the evolving digital landscape, setting the stage for continued growth and evolution.