In 2019, as a retailer, a D2C brand, or a pricing expert; if you heard the statistic that, in 2022, 64% of consumers will make regular purchases directly from brands, you’d likely wonder what could possibly take place in between those years for D2C shopping to become the majority choice for consumers. Direct-to-consumer, commonly called D2C, has jumped leaps and bounds in the last few years thanks to the traditional relationship between brand and retailer experiencing a reckoning with covid-19 lockdowns and closures that spanned two years.

In essence, the new face of D2C e-commerce was born out of a need for survival amongst brands, from tech to fashion, who were staring down the barrel in 2020 with closed retailers, supply chain issues and sitting stock. On the other end, stay-at-home consumers were searching for a way to receive goods directly to their homes. Today, D2C sales, including established brands and digital natives, are estimated to reach $182.6 billion in 2023 and, overall, D2C sales have increased by more than 36% from 2020 - 2022 in the US. Despite these successes, D2C - both online and offline - has also suffered from the global inflation crisis of 2022 that left brands contending with 10.1% inflation in the UK, 6.1% in France and a 31.7% increase in energy prices across the EU.

Facing increased competition, residual inflation, and a crackdown on sustainability practices, how does D2C fare for 2023? As we explore this growing sector of global e-commerce, Omnia looks to paint a portrait of its current state, as well as our predictions and expectations for the year ahead.

Established brands will dominate revenue in 2023, showing the major shift big brands have made to D2C

Despite showing impressive growth over the last few years, revenue for digitally-native vertical brands (DNVBs) will take a backseat to the more established brands that have made the move to D2C in recent years. In 2023, digitally-native brands are expected to earn $44.6 billion in revenue while established brands will earn much larger revenues, taking home $138 billion. In 2024, these numbers are expected to rise to $51 billion and $161 billion respectively. However, that doesn’t mean any less focus should be placed on the digital side of a brand’s sales stream.

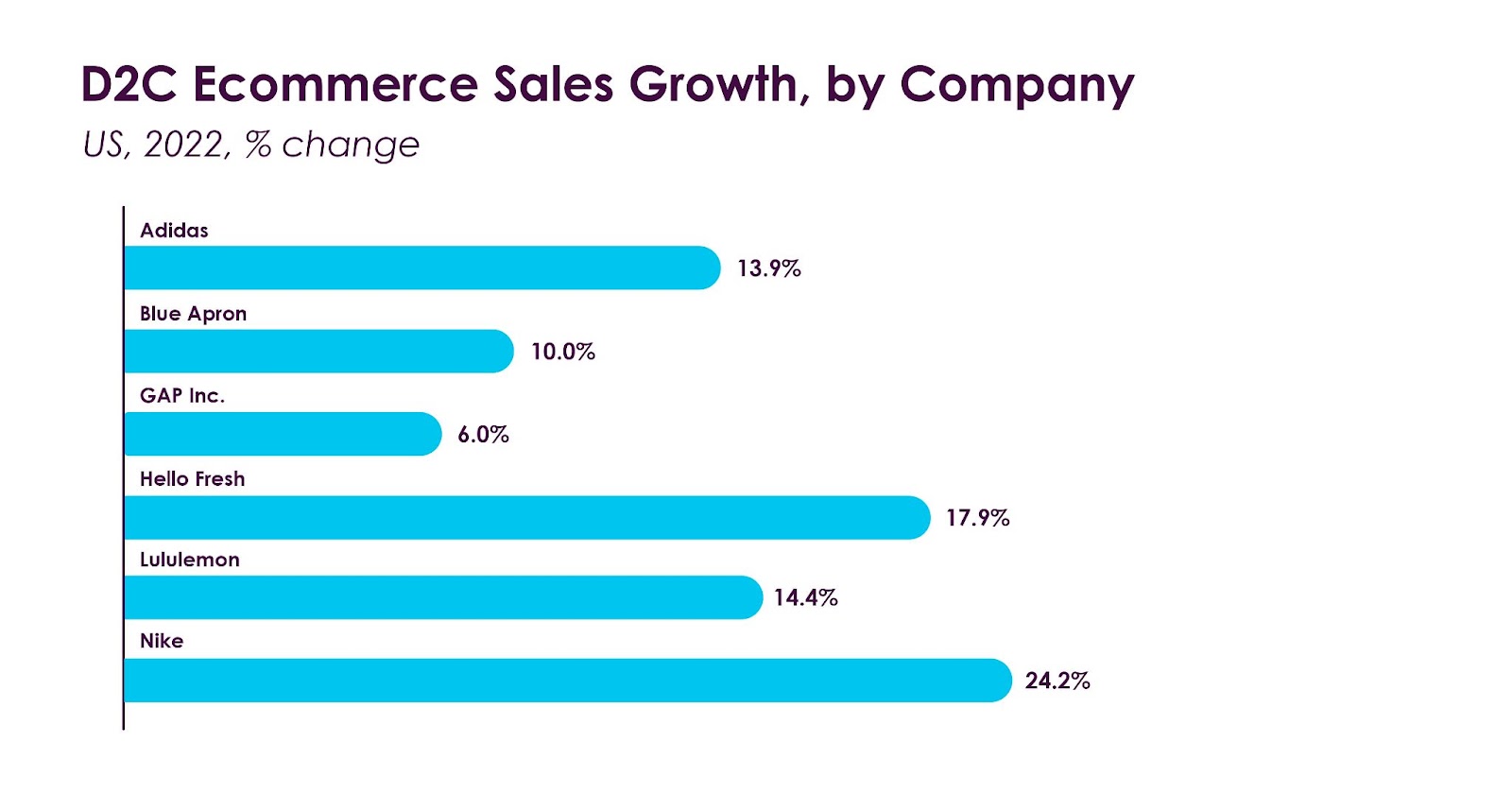

Although it is notable to see how well digitally-native brands are doing in the retail landscape, it is more noteworthy to see just how many established brands have made the move to D2C while some have circumvented the retailer route altogether at inception. Tech and home appliance brands like JBL, Phillips, Dyson, Bosch, and Miele, and sports brands like Nike, The North Face, Patagonia, New Balance and Under Armour have gone D2C - and these are just a handful of international brands that are making the move.

In Europe alone, D2C e-commerce has grown by 23% between 2021-2022, with Germany leading the way as it remains Europe’s most sophisticated nation regarding logistics, infrastructure and a supply chain network. In addition, 57% of multinational companies worldwide gave “significant financial investment” in their D2C strategy, while another 31% added “moderate investment”. In the US, the amount of D2C brand consumers are set to increase to 111 million shoppers in 2023, making up 40% of their population. Globally, D2C-specific shoppers are at 64%, up 15% from 2019.

Source: Insider Intelligence - D2C Brands 2022

Talk to one of our consultants about dynamic pricing.

Why more consumers are choosing D2C over retailers

When we see brands experiencing double-digit growth in their D2C channels, we know it’s because consumers have been making a conscious and active decision to go to the brand they love and trust directly.

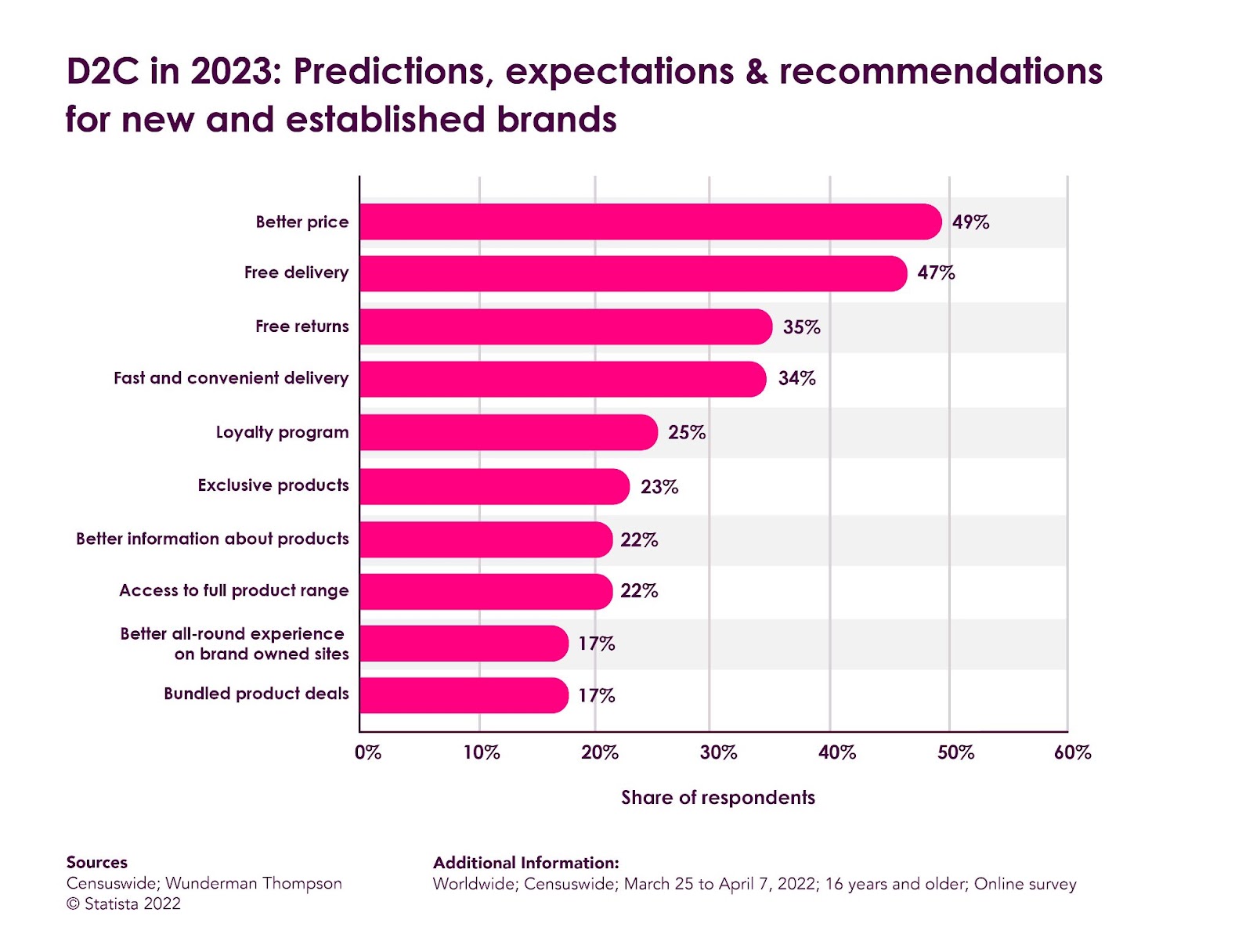

According to Statista, the leading reason consumers choose to shop directly from a brand, at 49%, is better pricing. In second place is free delivery at 47% and free returns at 35% in third place. Free delivery and returns were made industry-standard by Amazon before the covid-19 pandemic arrived, and have become the expectation of most consumers who specifically choose online shopping over a retailer for the reason of convenience and speed.

Source: Statista 2023

However, despite what many consumers think that they are getting a cheaper price directly from a brand, this is often not the case, which is why brands need a thorough dynamic pricing tool to offer a better price - not always the cheaper one - for the brand’s consistent growth.

As Omnia`s pricing data show, the necessity for a dynamic pricing solution is twofold: Brands have to contend with their entire retailer network. On average, a brand’s product will be sold by more than 1,000 shops on multiple marketplaces and comparison shopping engines in a national market, which the D2C channel must compete with. Secondly, prices are volatile; meaning that on average the lowest market price for a third of all products for any assortment will either increase or decrease on a daily basis. A dynamic pricing tool gives a brand the ability to react to market changes and consumer demands. The need for market insight is, therefore, vital for a brand.

D2C in 2023: In the face of increased competition, new brands will need to find a way to stand out

Gymshark, a UK-based sports apparel brand founded at first, in 2012, to digital customers only, has been labelled as a “challenger brand” for one simple reason: It’s found success in creating products around neglected areas within sportswear; one of them being the interests of the everyday gym-goer, instead of the successes of famous athletes. Nike, Adidas and Reebok, who have largely encompassed their ethos, identity and marketing around the famous athlete, from Rafael Nadal to Shaquille O’Neal to Cristiano Ronaldo, have peddled the dream of sporting victories to billions of consumers who - for the most part - can’t or won’t achieve that level of sporting success; although it is nice to fantasise.

Instead, Gymshark looked to focus their communication and overall identity on the wants and needs of the daily sport-lover and gym-goer who has a 9-to-5, or a family at home. In addition, the brand has focused on creating gym wear that isn’t only for model-like physiques or for fully able-bodied consumers. The online store shows people one would actually be sharing the leg press machine - not Tiger Woods. Now valued at €1.39 billion only a decade after its inception, the lesson that Gymshark can offer longstanding brands with a D2C channel is to not tell consumers to challenge the status quo with sharp taglines (“impossible is nothing”; “just do it”) but to actually do it themselves.

By 2025, the sportswear market across the globe will be valued at €395 billion, with a growth rate of 8-10 percent, showing just how much potential there is within the market to rise above the fray. “Activewear start-ups have found success by creating hyper-specialised products and marketing to local communities first,” reports Business of Fashion.

Not dissimilar to Gymshark, Off-White, the brand created by Virgil Abloh, learnt to fill an almost non-existent high-fashion-meets-streetwear gap. The creative director sadly passed away in 2021, however, his vision for meeting a misunderstood or neglected part of the streetwear market caught the attention of Louis Vuitton which led to his appointment as the luxury brand’s menswear artistic director in 2018. Off-White is still in production today.

“In a large part, streetwear is seen as cheap. What my goal has been is to add an intellectual layer to it and make it credible,” said Virgil. Strategic partnerships are also part of Off-White’s game plan to succeed in this niche, collaborating with both ends of the spectrum - from Jimmy Choo to Levi’s to Sunglass Hut to Nike.

Whether a brand is within the activewear or luxury category or not, we see opportunities for D2C players to focus on a niche in their segment or, like Gymshark and Off-White, look at the needs of consumers buying from those categories to see where they aren’t being met.

How D2C brands can prioritise long-term success and growth in 2023

Rely less on digital marketing spending for growth

In the early years of Facebook and Instagram, it was easy for brands to rely on sizeable marketing budgets to push growth. As consumers consumed content that was both organic and paid for, brands could rely on these platforms for sales and awareness. In addition, digital marketing on these channels used to be more affordable than it is today: On average, the cost per impression (reaching one person equals one impression) on Facebook cost $14.9 in 2021 versus $7.8 in 2019.

The cost to advertise also gets more expensive if there are more ads within a segment, making the increasing competition among D2C brands in food, clothing, or tech even more costly. The smarter alternative to funnelling funds into digital marketing is to have an all-rounded approach that involves social media with user-generated content, tips and “how-to” video content; strategic partnerships with brand ambassadors; personalised email marketing and subscriptions; as well as omnichannel in-store experiences. How D2C brands spend money to acquire customers matters over the long term with strategic, disciplined spending being better over the long term.

Focus on quality customer data

British mathematician Clive Humby said in 2006 that “Data is the new oil”, which is a statement that has proven to be true over the last few years. Research firm Magna Global found in a study they conducted that 83% of consumers are willing to share data - such as retail preferences, location, age, and marital status - to access discounted or personalised services. In addition, McKinsey reports that 80% of consumers want personalisation from retailers, which is a lesson the D2C sector could learn using customer data. Using quality customer data, D2C brands can build stronger relationships with customers, based on their personal preferences, when it comes to new product launches, sales, returns and delivery, and more. D2C can also optimise pricing and product assortment, as well as help brands understand the customer journey online.

Hire the right talent

Finding and retaining quality talent will be key to achieving long-term D2C success. From branding to e-commerce to digital to customer experience (CX/UX), having professionals and experts in these arenas is a non-negotiable point. Firstly, companies can look to see who, in the team, has the knowledge, credentials and skills to push forward the D2C agenda while offering them leadership positions or promotions. Another way to secure strong talent is to acquire professionals from existing scale-ups that have shown to be strong competitors in the market.

First-party data and underserved niche markets will be D2C’s best friends in 2023

Over the last three years since D2C experienced its most growth, we’ve been pleasantly surprised at the sector’s resilience, considering it is up against e-retailer and marketplace behemoths like Amazon, eBay, Bol.com, Walmart, and Target, as well as social commerce marketplaces under the Meta title. Both brands and consumers have shown an almost stubborn competitiveness in forging their own way within retail and e-commerce.

However, 2023 will not come without its challenges for D2C brands: Gaining and implementing strategies with first-party customer data will become more vital for growth while Apple and government regulators work to make third-party data a thing of the past. In addition, as the competition increases within D2C, brands will have to find ways to rise above the fray to stand out. In categories like skincare, beauty, or sports apparel where mostly established brands own the customer, new and emerging D2C brands should grab underserved niche markets by the horns.